Why should I choose AnalystNotes?

Simply put: AnalystNotes offers the best value and the best product available to help you pass your exams.

Basic Question 1 of 17

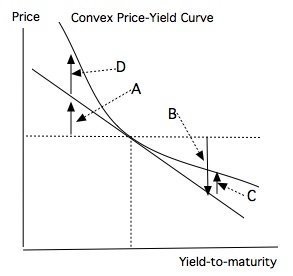

Refer to the following price-yield curve.

The estimated changes due to duration are represented by ______.

User Contributed Comments 2

| User | Comment |

|---|---|

| msusolar | can anybody explain? |

| CFAMay2022 | A&B reps changes in price due to change in YTM/slope of the tangent line (rather than actual changes on curve) |

I am using your study notes and I know of at least 5 other friends of mine who used it and passed the exam last Dec. Keep up your great work!

Barnes

Learning Outcome Statements

calculate and interpret convexity and describe the convexity adjustment

calculate the percentage price change of a bond for a specified change in yield, given the bond's duration and convexity

CFA® 2025 Level I Curriculum, Volume 4, Module 12.