Why should I choose AnalystNotes?

Simply put: AnalystNotes offers the best value and the best product available to help you pass your exams.

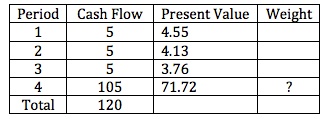

Basic Question 3 of 10

Consider a four-year, 5% annual coupon payment bond. Its yield to maturity is 10% and its price is 84.16 per 100 of par value.

B. 0.7172

C. 0.8522

To calculate Macaulay duration, what should be the weight of the last payment of 105?

A. 0.8750

B. 0.7172

C. 0.8522

User Contributed Comments 1

| User | Comment |

|---|---|

| janglejuic | 71.72 / (4.55+4.13+3.76+71.72) |

I was very pleased with your notes and question bank. I especially like the mock exams because it helped to pull everything together.

Martin Rockenfeldt

Learning Outcome Statements

describe the relationships among a bond's holding period return, its Macaulay duration, and the investment horizon

define, calculate, and interpret Macaulay duration

CFA® 2026 Level I Curriculum, Volume 4, Module 10.