Seeing is believing!

Before you order, simply sign up for a free user account and in seconds you'll be experiencing the best in CFA exam preparation.

Basic Question 3 of 10

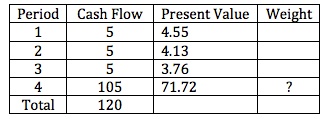

Consider a four-year, 5% annual coupon payment bond. Its yield to maturity is 10% and its price is 84.16 per 100 of par value.

B. 0.7172

C. 0.8522

To calculate Macaulay duration, what should be the weight of the last payment of 105?

A. 0.8750

B. 0.7172

C. 0.8522

User Contributed Comments 1

| User | Comment |

|---|---|

| janglejuic | 71.72 / (4.55+4.13+3.76+71.72) |

Your review questions and global ranking system were so helpful.

Lina

Learning Outcome Statements

describe the relationships among a bond's holding period return, its Macaulay duration, and the investment horizon

define, calculate, and interpret Macaulay duration

CFA® 2025 Level I Curriculum, Volume 4, Module 10.