Seeing is believing!

Before you order, simply sign up for a free user account and in seconds you'll be experiencing the best in CFA exam preparation.

Basic Question 0 of 11

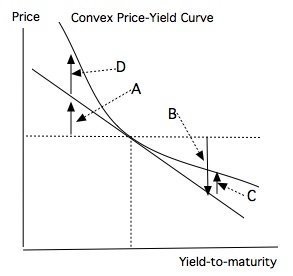

Refer to the following price-yield curve.

The estimated changes due to duration are represented by ______.

User Contributed Comments 2

| User | Comment |

|---|---|

| msusolar | can anybody explain? |

| CFAMay2022 | A&B reps changes in price due to change in YTM/slope of the tangent line (rather than actual changes on curve) |

I just wanted to share the good news that I passed CFA Level I!!! Thank you for your help - I think the online question bank helped cut the clutter and made a positive difference.

Edward Liu

Learning Outcome Statements

describe arbitrage pricing theory (APT), including its underlying assumptions and its relation to multifactor models;

define arbitrage opportunity and determine whether an arbitrage opportunity exists;

calculate the expected return on an asset given an asset's factor sensitivities and the factor risk premiums;

CFA® 2025 Level II Curriculum, Volume 5, Module 40.