- CFA Exams

- 2026 Level I

- Topic 2. Economics

- Learning Module 7. Capital Flows and the FX Market

- Subject 2. Exchange Rate Regimes

Seeing is believing!

Before you order, simply sign up for a free user account and in seconds you'll be experiencing the best in CFA exam preparation.

Subject 2. Exchange Rate Regimes PDF Download

The exchange rate regime is the way a country manages its currency in relation to other currencies and the foreign exchange market.

An ideal currency regime would have three properties:

- The exchange rate between any two currencies would be credibly fixed.

- All currencies would be fully convertible.

- Each country would be able to undertake fully independent monetary policy in pursuit of domestic objectives, such as growth and inflation targets.

However, these conditions are not consistent. A country cannot have a fixed exchange rate and fully convertible currency without giving up its ability to implement independent monetary policy.

In a flexible exchange rate regime, the exchange rate is determined by the market forces of supply and demand, and therefore fluctuates freely in the market. The central bank intervenes in the foreign exchange market only to smooth temporary imbalances. The advantages are that the exchange rate reflects economic fundamentals at a given point in time and governments are free to adopt independent monetary and fiscal policies. However, exchange rates can be extremely volatile in this regime.

A fixed exchange rate is an exchange rate that is set at a determined amount by government policy. The distinguishing characteristic of a fixed rate, unified currency regime is the presence of only one central bank with the power to expand and contract the supply of money. Those linking their currency at a fixed rate to the U.S. dollar or the euro are no longer in a position to conduct monetary policy. They essentially accept the monetary policy of the nation to which their currency is tied. They also accept the exchange-rate fluctuations of that currency relative to other currencies outside of the unified zone.

In practice, most regimes fall between these extremes. The type of exchange rate regime used varies widely among countries and over time.

No Separate Legal Tender

In this regime a country does not have its own legal tender. There are two sub-types:

- Dollarization. The country uses another country's currency as its domestic currency. The benefit is the elimination of exchange rate fluctuations. However, this leads to the loss of monetary policy autonomy.

- Monetary union. In this case a group of countries share a common currency, e.g., the European Union and the euro.

Currency Board System

The monetary authority is required to maintain a fixed exchange rate with a foreign currency. Its foreign currency reserves must be sufficient to ensure that all holders of its own currency can convert them into the reserve currency. That is, the monetary authority will only issue one unit of local currency for each unit of foreign currency it has in its vault.

The major benefit is currency stability and the main drawback is the loss of ability for the country to set its own monetary policy.

Fixed Parity

The country tries to keep the value of its currency constant against another country but it has no legal obligation to do so. This is also known as the pegged exchange rate system. There can be a very small percentage allowable deviation (band) on both sides of the rate.

Target Zone

This is a fixed parity with a somewhat wider band.

Crawling Peg

In this case, the exchange rate is fixed and then adjusted periodically to keep pace with the inflation rate.

Crawling Band This is initially a fixed parity, followed by widening band around the central parity. It is used to gradually exit from the fixed parity.

Managed Float

A country's exchange rate is adjusted based on the country's internal or external targets.

Independently Float

In this case, the market determines the exchange rate.

Exchange Rates and the Trade Balance

Countries that attract a net inflow of foreign capital tend to run current account deficits. The U.S. is an example. In general, a trade deficit (surplus) has to be offset by a capital account surplus (deficit). That is, a current account deficit implies a capital account surplus.

This relationship shows that a trade surplus is equal to the sum of public and private savings. A country saves more than enough to fund its investment (I) in plants and equipment. If a country runs a trade deficit, it has to rely on foreign capital to finance its investment (a capital surplus).

Now we analyze the impact of the exchange rate on trade and capital flows.

The Elasticities Approach

This approach emphasizes price changes as a determinant of a country's balance of payments and exchange rate.

The exchange rate is an important price in an economy. When a country's currency depreciates, domestic goods become relatively cheaper and foreign goods relatively more expensive in the global market. Hence, we would expect exports to rise and imports to decline. The elasticities approach considers the responsiveness of imports and exports to a change in the value of a country's currency.

For example, if import demand is highly elastic, a depreciation of the domestic currency will cause a disproportionate decline in the country's imports.

The Marshall-Lerner condition states that a depreciation of domestic currency can improve a country's balance of payments only when the sum of the demand elasticity of exports and the demand elasticity of imports exceeds unity.

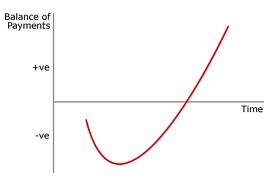

The J-Curve is an observed phenomenon.

What is observed is that, following a depreciation or devaluation, a country's balance of payments worsens before it improves. This is because, in the short-run, exports and imports volume does not change that much, so that the price effect dominates, leading to a worsening of the current account.

Absorption Approach

This approach assumes that prices remain constant and emphasizes changes in real domestic income. Hence, the absorption approach is a real-income theory of the balance of payments.

Absorption refers to the total goods and services taken off the market domestically. In other words, absorption equals the sum of consumption plus investment.

Whether a currency depreciation can improve the current account (then the balance of payments) depends on its effect on national income and on domestic expenditure (absorption).

- On the supply side, effective depreciation requires idle resources in the economy.

- On the demand side, effective depreciation requires the Marshall-Lerner condition to be met.

User Contributed Comments 7

| User | Comment |

|---|---|

| vatsal92 | - Flexible/Independent Float - Determined by market forces. - Fixed - Determined by government policy. - Dollarization - Another country's currency as its domestic currency. - Monetary Union - Group of countries sharing a common currency. - Currency Board Arrangement  Explicit commitment to exchange domestic currency for a specified foreign currency at a fixed exchange rate. - Conventional Fixed Peg Arrangement  Country pegs its currency within margins of +/- 1% versus another currency. - Pegged Exchange Rates within Horizontal Bands/Target Zone - Margins are wider. - Crawling Peg - Exchange rate is fixed, and adjusted periodically for inflation. - Crawling Band - Initially a fixed parity, followed by widening band around the central parity. This is used to gradually exit from fixed parity. - Managed Float - Exchange rate adjusted based on country's internal or external targets. |

| Wassimes95 | can someone tell me what is T, G and S in the the first formula |

| blackspy18 | taxes, government spending, and savings. if you are asking this on the last section you should probably go back and start at the beginning... |

| Fabulous1 | Made my day |

| choas69 | @wassimes95 you cant start studying halfway, please go through the first topics til lasts and keep ethics for last. |

| unknown | @vatsal92 Cheers |

| sant92 | @wassimes95 hereT stands for tax,G for government and S for savings.Hope this will help |

Your review questions and global ranking system were so helpful.

Lina

My Own Flashcard

No flashcard found. Add a private flashcard for the subject.

Add