- CFA Exams

- 2026 Level II

- Topic 9. Portfolio Management

- Learning Module 37. Economics and Investment Markets

- Subject 5. Equities and the Equity Risk Premium

Seeing is believing!

Before you order, simply sign up for a free user account and in seconds you'll be experiencing the best in CFA exam preparation.

Subject 5. Equities and the Equity Risk Premium PDF Download

Equities tend not to pay off in bad times. That is, the consumption hedging properties of equities are poor. This is why investors will demand an equity risk premium. In other words, the covariance between risk-averse investors' inter-temporal rates of substitution and the expected future prices of equities is highly negative, resulting in a positive and large equity risk premium. This is the case because, in good times, when equity returns are high, the marginal value of consumption is low. Similarly, in bad times, when equity returns are low, the marginal value of consumption is high. Holding all other factors constant, the larger the magnitude of the negative covariance term, the larger the risk premium.

A distinct feature of equity investment is uncertainty about and time variation in future equity cash flows (dividends). This is why investors would expect the equity risk premium to be larger than the credit premium.

The equity risk premium and the credit premium will tend to be positively correlated over time and will tend to be influenced by the business cycle in similar ways.

Corporate profitability can lead an economy out of recession as well as into it. The type of product sold or service provided by a company can have a big impact on earnings and equity performance over the business cycle. Companies that are in cyclical sector or produce durable goods are sensitive to the business cycle. When bond and equity investors are expecting an economic downturn, they may sell the equities and bonds issued by such companies in favor of those financial securities issued by companies whose earnings are less sensitive to economic conditions.

Valuation Multiples

Analysts use valuation multiples to compare equities.

- Trailing P/E: Price/Last Year's EPS

- Leading P/E: Price/Estimated Future EPS

- P/B: Price/Book Value

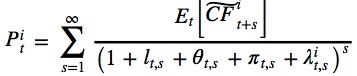

How does an analyst ascertain if the P/E (or P/B) is high or low? One approach is to consider a few economic factors. Remember the general pricing equation for equities?

For example, a high P/E could be the result of the following factors:

- An increase in the expectation of future real earnings growth (the numerator)

- Falling real interest rates (lt,s)

- A fall in inflation expectations (θ t,s)

- A decline in uncertainty about future inflation (πt,s)

- A fall in the equity risk premium (λ t,s)

All of these factors will be influenced by the business cycle (e.g., P/E tends to rise during periods of economic expansion).

Investment Strategy

The business cycle can affect the relative performance of different types of equity.

Growth stocks tend to trade with a high P/E and a very low dividend yield. When the economy is expanding they tend to outperform value stocks.

Value stocks tend to trade with a low P/E and a high dividend yield. They tend to outperform growth stocks when the economy is in recession.

Small-stock companies tend to have less-diversified earnings streams and have more difficulty in raising financing, particularly during recessions. They will thus be less able to weather economic storms and tend to underperform large stocks in difficult economic conditions. Therefore we should expect investors to demand a higher equity premium on small stocks relative to large stocks and the premium should rise in recessions.

Cyclical companies are expected to have a higher volatility in the growth rate of earnings relative to non-cyclical companies. During recessions, cyclical companies are likely to experience sharp declines in earnings, more so than non-cyclical companies. Investors should thus assign a higher equity risk premium to cyclical companies. In contrast, while coming out of a recession, cyclical companies are likely to generate higher earnings growth relative to non-cyclical companies.

User Contributed Comments 0

You need to log in first to add your comment.

I was very pleased with your notes and question bank. I especially like the mock exams because it helped to pull everything together.

Martin Rockenfeldt

My Own Flashcard

No flashcard found. Add a private flashcard for the subject.

Add