- CFA Exams

- 2026 Level I

- Topic 6. Fixed Income

- Learning Module 13. Curve-Based and Empirical Fixed-Income Risk Measures

- Subject 2. Key-Rate Durations

Why should I choose AnalystNotes?

Simply put: AnalystNotes offers the best value and the best product available to help you pass your exams.

Subject 2. Key-Rate Durations PDF Download

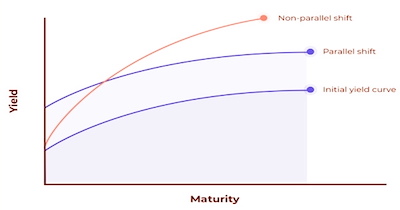

It is important to distinguish interest rate risk from yield curve risk.

The interest rate risk is the sensitivity of a bond to parallel shifts of the yield curve.

The yield curve risk is a bond's sensitivity to changes in the shape of the yield curve.

Parallel shifts in the yield curve rarely occur. An analyst may want to measure the change in the bond's price by changing the spot rate for a particular key maturity and holding the spot rate for the other key maturities constant. The key rate duration is the sensitivity of the value of a bond to changes in a single spot rate, holding all other spot rates constant. There is a key rate duration for every point on the spot rate curve so there is a vector of durations representing each maturity on the spot rate curve.

The key rate duration presents an improvement to the effective duration because it gives the expected changes in price when the yield curve shifts in a manner that is not perfectly parallel. In other words, it measures a security's sensitivity to shifts at "key" points along the yield curve.

Why Use Key Rate Duration?

A financial analyst may want to know how the price of the callable bond is expected to change if benchmark rates at short maturities shift by a specific number of basis points, but longer maturity benchmark rates remain constant. This case would represent a flattening of the yield curve, given that the yield curve is upward sloping. For parallel shifts in the benchmark yield curve, key rate durations could indicate the same interest rate sensitivity as effective duration.

Interpretation of Key Rate Duration

Interpreting each key rate duration in isolation can be quite difficult. That is because, in practice, it's highly unlikely that a single point on the yield curve will exhibit an upwards or downwards shift while all other points remain constant. For this reason, analysts tend to compare key rate durations across the curve.

User Contributed Comments 0

You need to log in first to add your comment.

I used your notes and passed ... highly recommended!

Lauren

My Own Flashcard

No flashcard found. Add a private flashcard for the subject.

Add