- CFA Exams

- 2026 Level I

- Topic 6. Fixed Income

- Learning Module 11. Yield-Based Bond Duration Measures and Properties

- Subject 1. Modified Duration

Why should I choose AnalystNotes?

Simply put: AnalystNotes offers the best value and the best product available to help you pass your exams.

Subject 1. Modified Duration PDF Download

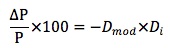

Modified duration shows how bond prices move proportionally with small changes in yields. Specifically, modified duration estimates the percentage change in bond price with a change in yield.

Di = yield change in basis points divided by 100

P = beginning price for the bond

V+ = the price if yield increases

V0 = the initial price

-Dmod = the modified duration for the bond

Di = yield change in basis points divided by 100

P = beginning price for the bond

Modified duration assumes that the price/yield relationship is a straight line. However, the price/yield relationship is convex, not linear. Suppose that the bond has an initial yield of Y0. A tangent line can be drawn to the price/yield relationship at Y0. The slope of the tangent line is related to the duration of the bond. If the yield falls to Y1, the price will rise to P1. Due to the linear assumption, the price change measured by duration is P2 - P0.

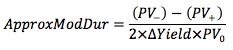

To approximate modified duration:

V- = the price if yields declines

V+ = the price if yield increases

V0 = the initial price

For example, consider a 9% coupon 20-year option-free bond selling at 134.6722 to yield 6%. If the yield is decreased by 20 basis points from 6.0% to 5.8%, the price would increase to 137.5888. If the yield increases by 20 basis points, the price would decrease to 131.8439. Thus: ApproxModDur = (137.5888 - 131.8439)/(2 x 134.6722 x 0.002) = 10.66. This tells you that for a 1% change in the required yield, the bond price will change by approximately 10.66%.

Macaulay duration is mathematically related to modified duration.

A bond with a Macaulay duration of 10 years, a yield to maturity of 8% and semi-annual payments will have a modified duration of: Dmod = 10/(1 + 0.08/2) = 9.62 years

User Contributed Comments 16

| User | Comment |

|---|---|

| yodaddy | I am using both Schweser and analystnotes' notes. According to Schweser, you dont need anything besides Effective Dur. --> IS EFFECTIVE DUR. the only thing needed... can i listen to schweser and ignore modified. |

| tamagoochi | DO NOT ignore modified duration - pretty good chance it will be tested. Check the L.O.S's. In fact, modified duration is more important than effective when figuring out most questions. |

| jayson | Effective duration and modified duration essentially give the same information - the percentage change in price for a 1% change in yield. The only difference is in the way the duration is calculated - modified duration is based on the first derivative of price with respect to yield whereas effective duration is based on estimating a change in price for a given change in yield in either direction, through use of pricing models, for example. The implication of this is that effective duration is more flexible in its usage, since it can deal with, for example, callable bonds more easily.A question could give you a value for modified duration or effective duration, and you would use each identically. |

| yodaddy | PROBLEM here is Schweser has ignored modified and has called modified dur, effective dur. ONly diff it says... you can use effective for any situation and also you get the same answer. I wanna smack Mr. Schweser in the head if thats not true and hes sending me into the exam with such ludicrous consequences. POST ME A FORUMLA if you can for MODIFIED. FOR EFFECTIVE......it is....for example:v- - v+ -------- 2(vo) x change in yield in decimalv- price when yield fell v+ opposite vo = price of bond HELP ME PLEASE thanks. |

| kalps | Mr Swhweser is money making machine with a near monopoly in the CFA materials business - he is clever and richer than any of us will eve rbe - so he can afford to produce rubbish notes - he has the power to do whatever he likes |

| Hyper | Duration increases with square root of maturity! |

| NillePet | Am i getting it right that mod. duration and effective duration are giving the same result? So it is the approx. change in price for a 100 Bps change in yield. But why is the result in the example of mod. duration stated in years then? |

| freyalam | Schweser doesn't ignore the modified duration. I'm doing the proQ test bank and questions about modified duration show up very often. |

| kondagadu | you cannot use modified duration for callable bonds .effective duration can be used for both callable and option-free bonds. |

| bidisha | I don't get how modified duration is different from normal duration? |

| bidisha | Never mind I get it. Normally used, the term duration IMPLIES modified duration. But technically, duration can be of 3 different kinds: modified, effective & Macaulay. |

| gill15 | Its hilarious. All this time writing about or thinking about if you should know this....you do understand it is ONE page not even 75% of one page that you have to read in the CFA curriculum book... |

| robertdole | Also, with callable bonds, the YTM is not reliable (because the issue may be called at any given point in time in the future, if the issuer can refund the debt at a cheaper price); so EffDur provides a more accurate read at price sensitivity given moves in the yield curve. |

| robertdole | ModDur and EffDur are looking at two different catalysts for bond price movements. |

| robertdole | p.545 in the CFAI books, reading 56. |

| nvallabh | Can someone help me understand.....with MACAULAY duration, the indication/output is measured in YEARS. While MODIFIED is a % change in bond price? Confusing! |

I just wanted to share the good news that I passed CFA Level I!!! Thank you for your help - I think the online question bank helped cut the clutter and made a positive difference.

Edward Liu

My Own Flashcard

No flashcard found. Add a private flashcard for the subject.

Add