- CFA Exams

- 2026 Level I

- Topic 6. Fixed Income

- Learning Module 11. Yield-Based Bond Duration Measures and Properties

- Subject 2. Money Duration and Price Value of a Basis Point

Why should I choose AnalystNotes?

Simply put: AnalystNotes offers the best value and the best product available to help you pass your exams.

Subject 2. Money Duration and Price Value of a Basis Point PDF Download

Modified duration measures the percentage price change of a bond to a change in its yield-to-maturity. Money duration measures the absolute price change.

To calculate absolute price change:

In the U.S., money duration is called dollar duration. It is the approximate dollar change in a bond's price for a 100 basis point change in yield.

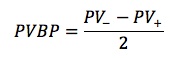

The price value of a basis point (PVBP) is the absolute change in the price of a bond for a one basis point change in yield. It is simply the money duration of a bond for a one basis point change in yield.

Example

Scott Marsh from Mass Avenue Research Management purchased a bond for a price of 93.555. This bond has a coupon of 14.70% and a modified duration of 3.00. Given market interest rates of 10.00% and a change in market rates of -66 basis points, what is the price value of a basis point?

The answer is the modified duration x 1 basis point x bond price or 3.00 x .0001 x 93.555 = $0.0281

Note: The other information has been placed into this question as a distraction. Don't be fooled by extraneous data!

To calculate PVBP:

P- is the full price calculated by lowering the yield-to-maturity by one basis point.

P+ is the full price calculated by raising the yield-to-maturity by one basis point.

User Contributed Comments 9

| User | Comment |

|---|---|

| kalps | You have screwed up in the first calculation - the naswer is 0.280665 - did you hurry the las part of these notes up or something ??? |

| shasha | kalps: the answer for the first calculation is correct. Personaly, i like the example, it tells you how to use PVBP and its meaning by making some "noise" in the question. the last two examples do seem redundant, but didn't hurt me. |

| shasha | one more, i'd say the last two examples were trying to tell us: "percentage price change for 1BP" = duration/100, 'coz duration is actually percentage price change for 100BP. in the example, the percentage price change for 1BP is 0.1066 percent. have to say explanation to this LOS is not as beautiful as others. |

| zax4 | always second guess Kalps |

| AusPhD | I have never heard better advice |

| uberstyle | Agreed. I started ignoring his comments after he went 0 for 10. |

| steved333 | HAhaha!! You guy are harsh! |

| joe10001 | LOL Don't give up kalps! |

| khalifa92 | Remember Dollar duration: 0.01 * Modified Duration * Full price PVBS: 0.0001 * Modified Duration * Full price |

I was very pleased with your notes and question bank. I especially like the mock exams because it helped to pull everything together.

Martin Rockenfeldt

My Own Flashcard

No flashcard found. Add a private flashcard for the subject.

Add