- CFA Exams

- 2026 Level II

- Topic 9. Portfolio Management

- Learning Module 37. Economics and Investment Markets

- Subject 3. The Yield Curve and the Business Cycle

Why should I choose AnalystNotes?

Simply put: AnalystNotes offers the best value and the best product available to help you pass your exams.

Subject 3. The Yield Curve and the Business Cycle PDF Download

Short-Term Interest Rate and the Business Cycleshort-term nominal interest rate = short-term real interest rate + expected inflation rate

prt = policy rate at time t

lt = real short term interest rate

it = rate of inflation

i*t = target rate of inflation

Yt = the logarithmic level of actual GDP

Y*t = the logarithmic level of potential GDP

Short-term nominal interest rates are positively related to short-term real interest rates and inflation expectations.

As discussed in the last section, short-term nominal interest rates are positively related to the level and volatility of GDP growth.

The inflation environment is a key driver of short-term interest rates.

A responsible central bank usually bases its policy rate on the level of expected economic activity and inflation.

- If the nominal interest rates are considered too high, the central bank will cut its policy rate.

- If the nominal interest rates are considered too low, the central bank will raise its policy rate.

The Taylor rule suggests setting a central bank's policy rate as follows:

where:

prt = policy rate at time t

lt = real short term interest rate

it = rate of inflation

i*t = target rate of inflation

Yt = the logarithmic level of actual GDP

Y*t = the logarithmic level of potential GDP

Yt - Y*t is known as output gap. If it is positive, the economy is producing beyond its capacity and inflation is likely on the rise. If it is negative, unemployment may become an issue.

When inflation is close to the targeted rate and there is no output gap, the policy rate will be lt + it. This rate is referred to as the neutral policy rate. The neutral policy rate is not constant, however. It can vary with the level of real economic growth and with the expected volatility of that growth.

Other factors being equal:

- When inflation is above (below) the targeted level, the policy rate should be above (below) the neutral rate.

- When the output is positive (negative), the policy rate should be above (below) the neutral rate.

The policy rate can thus vary over time with inflation expectations and the economy's output gap.

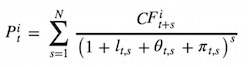

Conventional Government Bonds

This equation can be used to calculate the present value of any risk-free security.

θt,s is the expected inflation and πt,s is the risk premium for the uncertainty of the expected inflation. πt,s can be negligible for short-term government securities but it can become significant for long-term government bonds.

The break-even inflation (BEI) rate is defined as the difference between the yield on a zero-coupon default-free nominal bond and the yield on a zero-coupon default-free real bond of the same maturity. It incorporates both θt,s and πt,s.

The Default-Free Yield Curve and the Business Cycle

The yield curve levels are positively related to the level of economic activity and views of future inflation.

The slope of the yield curve is influenced by the magnitude of the risk premium. The risk premium will generally rise with the maturity of these bonds because longer-dated government bonds tend to be less negatively correlated with consumption and therefore represent a less useful consumption hedge for investors.

Other factors can also affect the slope of the yield curve. For example, during a recession a central bank will tend to lower its short-term rates so the slope will increase. Inflation expectations, business cycle, and policymaker decisions can all influence the shape of the yield curve.

User Contributed Comments 1

| User | Comment |

|---|---|

| davidt87 | this curriculum is all over the place. i definitely shouldve done this section before the currency section |

Your review questions and global ranking system were so helpful.

Lina

My Own Flashcard

No flashcard found. Add a private flashcard for the subject.

Add