- CFA Exams

- 2026 Level II

- Topic 6. Fixed Income

- Learning Module 27. The Arbitrage-Free Valuation Framework

- Subject 3. Valuing an Option-Free Bond with a Binomial Tree

Why should I choose AnalystNotes?

AnalystNotes specializes in helping candidates pass. Period.

Subject 3. Valuing an Option-Free Bond with a Binomial Tree PDF Download

If we are at some node in a tree, then the value at that node will depend on the future cash flows. Simply speaking, backward induction is a methodology to move backwards in the tree:

= 1/2 x (100 + 5) / (1 + 0.037031) + 1/2 x (100 + 5)/(1 + 0.037031) = 101.251.

- Determine the value at node 0, once you know the value at node 1.

- Determine the value of node 1, once you know node 2.

- ... until the root of the tree is reached.

Let's assume that values at the two nodes in year N+1 (i.e., VN+1,H and VN+1, L) are known with certainty. We need to calculate VN. We employ the backward induction methodology - discount VN+1,H and VN+1,L at rN (not rN + 1!) and find the mean of these discounted values to arrive at VN.

where

- VH = the bond's value at node N +1 for the higher 1-year rate.

- VL = the bond's value at node N+1 for the lower 1-year rate.

- C = coupon payment at node N+1.

- r = the 1-year rate at node N.

Example

Assume the following spot rate curve. We want to find a value of a 4-year 5% option-free bond, assuming 15% annual yield volatility.

We compare traditional valuation of option-free bonds with valuation using interest rate trees. Therefore, we start with the spot rate curve and perform traditional valuation first:

V = 5/(1.025) + 5/(1.032113)2 + 5/(1.038324)3 + 105/(1.043615)4 = 102.555

The bond should trade at 102.555% of par.

Now assume that based on the spot rate curve we construct the following binomial interest rate tree. Notice that interest rates at the end of year 4 are irrelevant, because there are no cash flows during year 5.

Next, we employ the backward-induction approach. We start with the maturity and discount both principal and cash flows to find values at each node until we reach the root of the tree. The value at the root should be equal to the arbitrage-free value that we have found above.

At each node we state the bond's value, obtained from the backward induction, the coupon to be paid at this node, and the one-period interest rate that is used for discounting of values at future nodes.

For example, let's demonstrate how we got the value of 101.251. At maturity the value of the bond equals its principal (100) plus coupon (5). We discount both principal and coupon from each of these two nodes:

V3,LLL = 1/2 x (V4, LLLH + C) / (1 + r3,LLL) + 1/2 x (V4, LLLL + C)/(1 + r3,LLL)

= 1/2 x (100 + 5) / (1 + 0.037031) + 1/2 x (100 + 5)/(1 + 0.037031) = 101.251.

We continue this procedure, going backwards until we reach the root, at which point V0 is the fair value of the bond 102.555. As expected, this is the same value that we obtained earlier, when we applied the traditional arbitrage-free valuation to the same option-free bond.

Calibrate the model: Valuing a non-callable bond with the binomial tree must replicate its market value.

Example

Assume the following information is given:

- The one year spot rate is 4.5%.

- Two-year, annual coupon bonds are selling at par and yield 4%.

- One-year interest rate volatility is 15%.

To determine the one-year forward rates, one year from now, consider the cash flows on the two year bond:

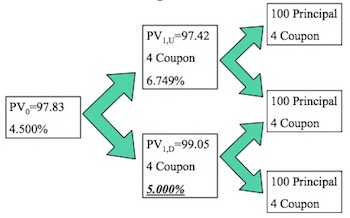

Guess an interest rate for the "down" scenario: 5%. The "up" interest rate is 0.05 e(.15)(2) = 6.749%.

Begin at the bond's maturity and work backward.

Discount by the assumed one-year interest rate:

- PV1,U = 104/1.06749 = 97.42

- PV1,D = 104/1.05 = 99.05

After calculating the values at time 1, include the coupon payment and discount to time 0. The value of the bond is the average present value:

PV0 = [(97.42+4)/1.045 + (99.05 + 4)/1.045]/2 = 97.83

Our interest rate process does not reproduce the two-year bond market value. Since the PV is too low, the guess of 5% is too high. Use trial-and-error (or a Solver) to find the correct rate: 2.97%.

Once the model is calibrated through two years, we can continue the process for three years:

- Keep the "calibrated" two year rates for the three-period tree.

- For each period, the unknown interest rate that we must determine is the one-year interest rate corresponding to all down movements.

- All other rates are related to this guess.

Assume that we have found all of the nodes needed for valuing a cash flow. Interest rate binomial tree is completed through the last payment date.

- Bonds can be valued using the completed tree.

- For option-free bonds, results should be identical to valuation using spot rates or implied forward rates.

- Bonds with options may also be valued using the tree.

Because of this feature and the feature of pricing option-free bonds equal to their equilibrium prices, the calibration model is referred to as an arbitrage-free model.

User Contributed Comments 6

| User | Comment |

|---|---|

| Oksanata | r is the rate of the previous year. There are 4 rates of year 3 in the example. Why they used r3,LLL? |

| Oksanata | got it..r is the 1-year rate @ NODE N |

| myron | The tree should generate arbitrage-free values for on-the-run issues of the benchmark security. This means that the value of these on-the-run issues produced by the interest rate tree must equal their market prices, which excludes arbitrage opportunities. Without this assumption, the model would not be able to price more complex callable and putable securities. |

| connor | The value of a bond at a given node on the binomial tree is the average of the PVs of the two possible values from the next period. At any node, the value of the bond depends on future cash flows and the one-period interest rate. Binomial, hence "equal weighting". |

| connor15 | Calibration of the model is performed so as to make model consistent with the current term structure. |

| cfaexaminee | The calibration method generates a binomial tree that is consistent with an estimated relationship between the variance of the upper and lower spot rates and yields a bond value that reflects the current term structure. |

I was very pleased with your notes and question bank. I especially like the mock exams because it helped to pull everything together.

Martin Rockenfeldt

My Own Flashcard

No flashcard found. Add a private flashcard for the subject.

Add